After over a decade of historically low interest rates, higher cash yields are a welcome development. Interest rates are higher across all cash instruments including many savings accounts, certificates of deposit, and money market funds. The federal funds rate has remained in a range of 5.25% to 5.50% since July of 2023.

And after the recent Fed meeting, Fed Chair Jerome Powell noted that it “will take longer than previously expected” to gain greater confidence that inflation is on the right path, implying that policy rates could stay higher for longer. Yet despite seemingly high rates of return on cash, as detailed below, cash is a very bad investment.

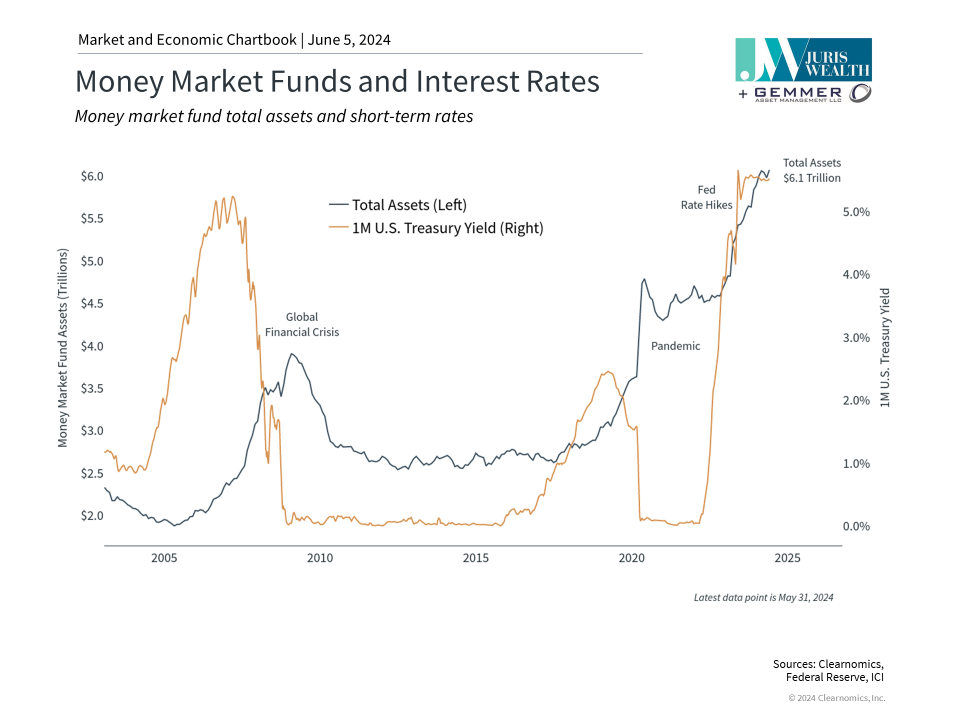

Huge flows into money market funds

People are plowing a lot of money into cash and cash-like investments. Money market funds have attracted record inflows with total assets reaching new all-time highs of $6 trillion. This is more than double the assets held in money market funds prior to the pandemic when interest rates were near zero.

Cash yields are negative when factoring in inflation

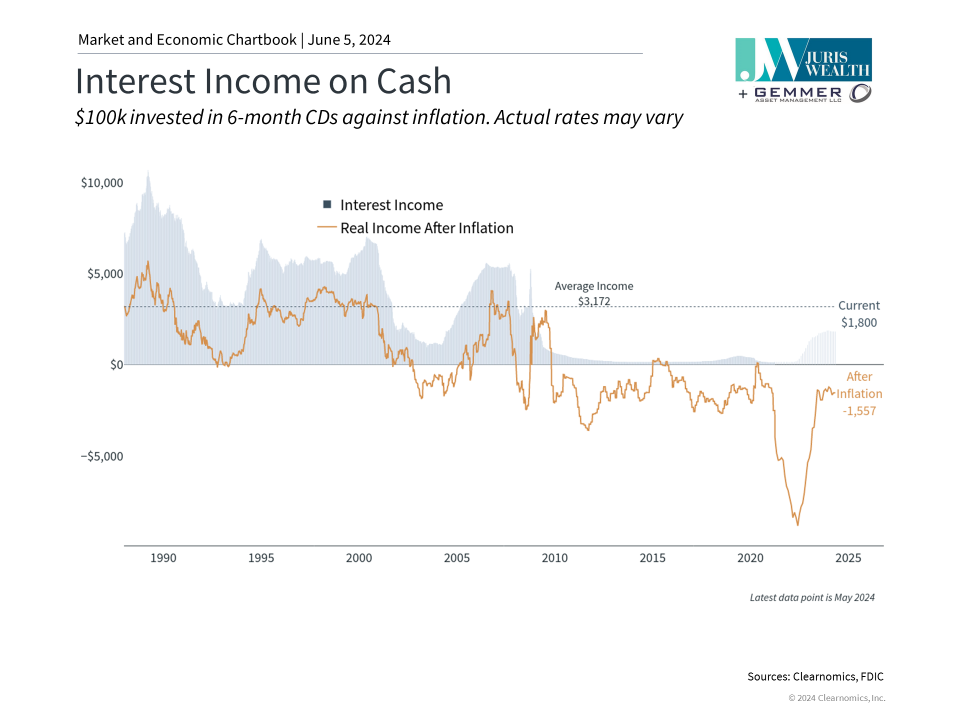

The first obvious problem with cash as an investment is the impact of inflation. Even if yields appear to be high, if you adjust for inflation, you may be losing purchasing power. The chart below shows (on the yellow line) the inflation adjusted income relative to the average 6-month CD rate.

It’s even worse after factoring in taxes

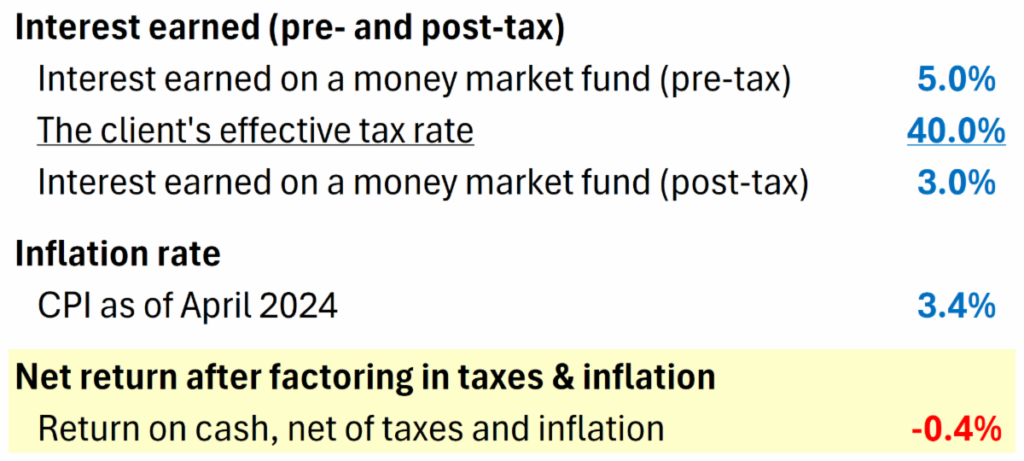

Interest income is taxed at the highest Ordinary Income rates, not more-favorable capital gains rates. Many of my clients have effective tax rates of 40% or higher. At a 40% tax rate, you’re only taking home 60% of that advertised interest rate: a 5% pre-tax interest rate means you’re earning just 3% after taxes. Factor in inflation, with the CPI currently above 3%, and again – you’re looking at a negative return, as illustrated below using current data (June 2024).

The single biggest (but least obvious) problem

While today’s higher levels of interest on cash may provide investors with some psychic security in the short term, the core issue is the massive potential opportunity cost of not deploying that cash into higher returning financial assets like stocks. While past performance is obviously not a guarantee of future results, the “equity risk premium” that is expected from stocks is several percentage points above the overall inflation rate.

In the short-term, you may be tempted to stay in cash for what looks to be something like a guaranteed 5% return, but compared to something closer to 10% (reflecting historical stock returns, with dividends reinvested), the difference in wealth creation is astonishing. Using returns on 3-month T-Bills as a proxy for what returns on cash would have been historically, just compare the wealth created (or not created) over the long term by buying stocks with your cash vs. holding cash (source).

Hold as much cash as you need to. But no more than needed. I know it feels great to be earning 5% or more on your cash deposits. But it’s false security for the long-term. I don’t miss the days of 0% interest on cash, but at least that gave us all the (healthy) prompt to do something better with our money than just sit on it!