In April of 1997, I ran the Boston Marathon. I was a 3L at Harvard Law. I wasn’t a runner. I had no business being on that course.

If you’ve been to law school, you know the strange shape of the third year — job lined up, bar exam looming, classes that can’t fire you. A rare window to take on a hard thing just to see if you can. A few of my classmates had run Boston in their 1L and 2L years. The idea stuck.

So in January, three months before the race, I started training. In Cambridge. In January. It was awful.

I had one goal for the race: to finish

Race day, I lined up as a bandit — no bib, no chip — and ran. I hit the wall around mile 22. I kept moving. Slowly. Painfully. More than 4 hours later I crossed the line.

That morning my roommate Alex woke up said: “I think I’ll run the marathon with you.” Alex hadn’t trained at all. But he was a gym rat, and in insane shape. The fact he needed ACL surgery didn’t faze him at all. We got a ride to the starting line together. He finished in three and a half hours, well ahead of me.

I didn’t care.

At every mile, somebody was faster. At every mile, somebody was slower. None of it mattered. I had set a goal. I had hit it.

There is always someone running faster

I think about that race when I talk to clients — especially the competitive athletes. They are wired to compete. That wiring follows them into their portfolios.

They look at the quarterly statement and ask: “Should we have had more in that fund? In that sector? In that geography?”

Every quarter, the answer is yes — for something. There is always a fund that did better. A sector that did better. A country that did better.

There will always be an investment doing best at any given moment. Always.

Just like at every mile of the marathon, there was always somebody faster than me. Always.

Investing is no different.

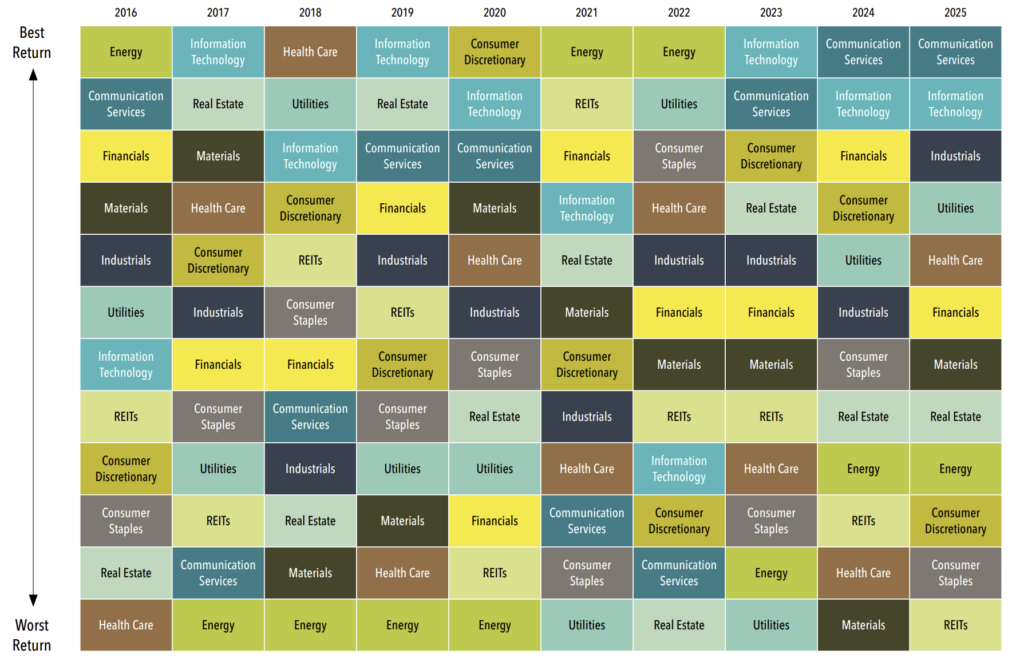

Equity sector returns, 2016-2025

Source: Dimensional Fund Advisors. See below for chart disclosures

Over the trailing ten years, no sector was a consistent outperformer. Not one.

Look at Energy as an example, it was the #1 sector in three of the last ten years — and the worst sector in four of them. Same sector. Same decade.

If you had spent the decade chasing last year’s winner, you would have spent the decade losing. There was nothing to catch up to.

The sectors are just an example of the futility of chasing the winners. We could take individual chip stocks, or crypto, or Gold. Whatever the partner two offices down is crowing about at the partner retreat. Name the investment that is currently sprinting to the finish.

Run your own race

Your race is not the partner two offices down. Not your brother-in-law’s hot stock. Not the fund on the cover of Barron’s. Not the runner flying past you at mile 12.

Your race is whether you cross *your own* finish line. That line is probably some version of this: a comfortable retirement, on your terms, that you do not outlive. Maybe parents cared for. Kids launched. The freedom to stop practicing when you are ready, not when you’re just too old to keep working.

If you cross that line, you’ve won. Ultimately, the only people you are racing are your future self and his bills.

My roommate Alex finished in three and a half hours. I finished much later. We both finished. From the perspective of the goal each of us had set — finish the Boston Marathon — we both won.

That is how to think about your portfolio.

Define the line.

Cross the line.

The rest is noise.

Chart disclosures: Chart disclosures: In USD. The annual returns are Russell 3000 Index Global Industry Classification Standard (GICS) sector returns. Real estate investment trusts (REITs) are shown as a separate category to illustrate their exclusion from certain funds. REITs are classified according to the GICS.

S&P/MSCI changed the GICS methodology after market close in September 2018 to rename “Telecommunication Services” to “Communication Services” and to reclassify a number of companies to that sector. Dimensional reports these changes in company membership to Communication Services starting in October 2018, but changes the name historically to Communication Services to maintain consistency.

Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes.

The GICS was developed by and is the exclusive property of MSCI and S&P Dow Jones Indices LLC, a division of S&P Global.

Sector Definitions:

Communication Services: Companies that provide telecommunication services, such as wire line, wireless, and internet access.

Consumer Discretionary: Companies that produce nonessential goods and services, such as automobiles, apparel, and leisure activities.

Consumer Staples: Companies that produce basic necessities like food, beverages, and household goods.

Energy: Companies involved in the exploration, production, refining, transportation, and marketing of oil, natural gas, and other energy sources.

Financials: Companies that provide financial services, including banks, insurance companies, and investment firms.

Health Care: Companies that provide health-care products and services, including pharmaceuticals, biotechnology, medical devices, hospitals, and health insurance.

Industrials: Companies that manufacture industrial goods, such as machinery, aerospace, construction materials, and chemicals.

Information Technology: Companies that design, develop, and sell computer hardware, software, and services.

Materials: Companies that produce basic materials, such as metals, chemicals, and forest products.

Real Estate: Companies engaged in real estate development and operation.

REITs: Companies known as real estate investment trusts, which own, operate, or finance income-producing properties.

Utilities: Companies that provide essential utilities, such as electricity, water, and natural gas.