As a wealth manager for lawyers, I see a number of mistakes so consistently that I thought I’d summarize the top 3 most common.

These mistakes aren’t random. They are not made because lawyers are careless or lack intelligence. The mistakes reflect how lawyers are sold to, how the profession thinks about money, and how a legal career is actually structured.

Letting the (tax) tail wag the (investment) dog

“Tax-advantaged” products are catnip for lawyers. The pitch for the investment product that leads with the tax advantage lands because the pain point is so clear: ordinary income is taxed at the highest rates, and meaningful legitimate tax deductions for W-2 and K-1 earners are scarce.

The tax benefit is often the key attribute lawyers are attracted to. When a lawyer is being sold a whole life insurance policy, a direct indexing strategy a tax-advantaged long-short fund, a tax-efficient real estate investment – or, God help us, a conservation easement – the siren song of tax savings does a lot of work in the lawyer’s head to convince them it’s a good (and even a “smart”) investment.

This is backwards. Investments should be evaluated from a number of different perspectives, but the first is simple: what’s the expected net return on investment? If that’s not where the sales pitch starts, run.

Think of tax advantages like a coupon. A coupon is a great reason to feel good about a purchase you were already going to make. It is a terrible reason to make the purchase in the first place. If the underlying product is overpriced or doesn’t fit, the coupon doesn’t save you.

Starting too late

Compounding interest over time is the most powerful force in a high earner’s financial life. It does not care how impressive your career arc is. It does not care how much money you make. It cares how long your money has been compounding.

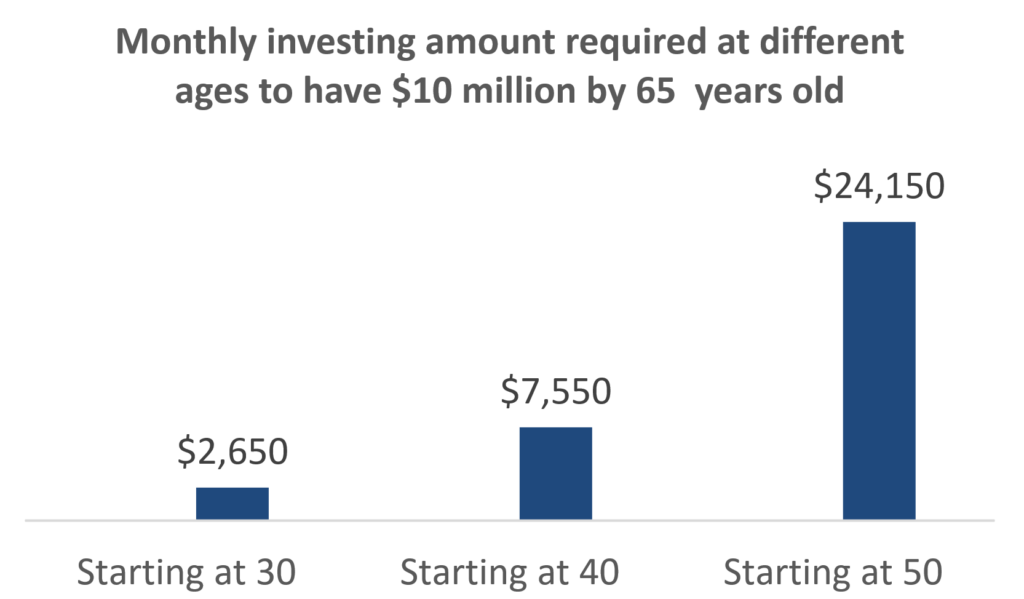

Take three lawyers of different ages: 30 years old, 40 years old and 50 years old. Each wants to accumulate $10 million by age 65. Below is a chart showing the amounts required to be invested on a monthly basis based on the age each starts if you assume a 10% annual compounding return.

See below for chart disclosures

If you start saving at 50 years old instead of 30 years old, you have to invest nearly ten times as much per month to end up in the same place.

This shows you the overwhelming power of time when investments compound. Ten years of compounding at the front end is worth more than twenty years of frantic saving at the back end.

The trap is that lawyers feel like they’re starting on time, because the income arrives late. Maybe you’re not making real money until you make partner. Partner happens in your mid-to-late thirties or your forties. So it feels reasonable to start the real saving then. Compound interest does not care what felt reasonable.

Listening to generic financial advice

I’ll give you two basic examples. Though there are plenty of others I could share.

The first example is the target date retirement fund. Have you ever gone to buy a suit and got the “one-size-fits-all” version? Of course not. You buy a suit that fits. If you wouldn’t buy a one-size-fits-all suit, why would you buy a one-size-fits-all investment? To be fair, target date funds are wonderful inventions, and I’ve advised clients to use them in certain contexts. But they are necessarily very simplistic: there is one fact that is deemed to be singularly relevant, the year in which you intend to retire. But that’s not the only thing you need to know about someone’s financial situation to determine an appropriate investment allocation. Things like your risk tolerance, the size of your existing assets, whether you have a pension, the stability of your income, your spending habits, your tax situation, whether you’re likely to inherit money, or whether you’re trying to build generational wealth all matter enormously.

The second is advice that comes out of personal finance media built for the median American household. Last week I wrote about Dave Ramsey’s bad advice to pay off a mortgage in fifteen years. Listening to Dave on this point could easily be a multi-million-dollar mistake. Pick your guru. Suze Orman. Clark Howard. There is a ton of good advice they offer. But not all of it applies to you. Generic advice assumes generic circumstances. Your circumstances are not very likely generic.

Chart disclosures: Assumes a 10% net annual compound return, with amounts invested monthly commencing at the ages indicated, in order to have a terminal value of $10 million at age 65. For illustrative purposes only. All investing involves the risk of loss.