Watch a man get into cold water

The cautious man wades into cold water inch-by-inch, gasping at each new step. While he believes he is controlling his discomfort, he is simply extending its duration. The same total amount of cold, stretched across more time — he’s just decided to suffer slowly. The man who simply jumps in is shocked once, and then he is swimming. The paradox: the move that feels reckless is the more efficient one. The careful move is what costs you. Call it the “caution tax”.

What does this have to do with lawyers and investing?

Investing your profit distribution

Take the young law firm partner with a $100,000 profit distribution. He has already decided it’s for long-term investing. The only question is whether to invest all at once or to spread the investment across some amount of time.

The careful lawyer hedges

This is an area where I believe our legal training works against us. We are paid to identify risk. We catch what other people miss. We are measured, careful with our words, careful with our decisions. In that context, we read the Wall Street Journal and The New York Times, and we watch CNBC. The Strait of Hormuz is blocked, the deficit is exploding, AI is going to revolutionize the world in ways we can’t imagine.

So OK, fine, we’ll get invested. But just in case there’s a market crash tomorrow, we hedge our bets a bit, and wade in. We’ll dollar cost average our $100,000 on a monthly basis over a year.

The significant cost of a cautious approach

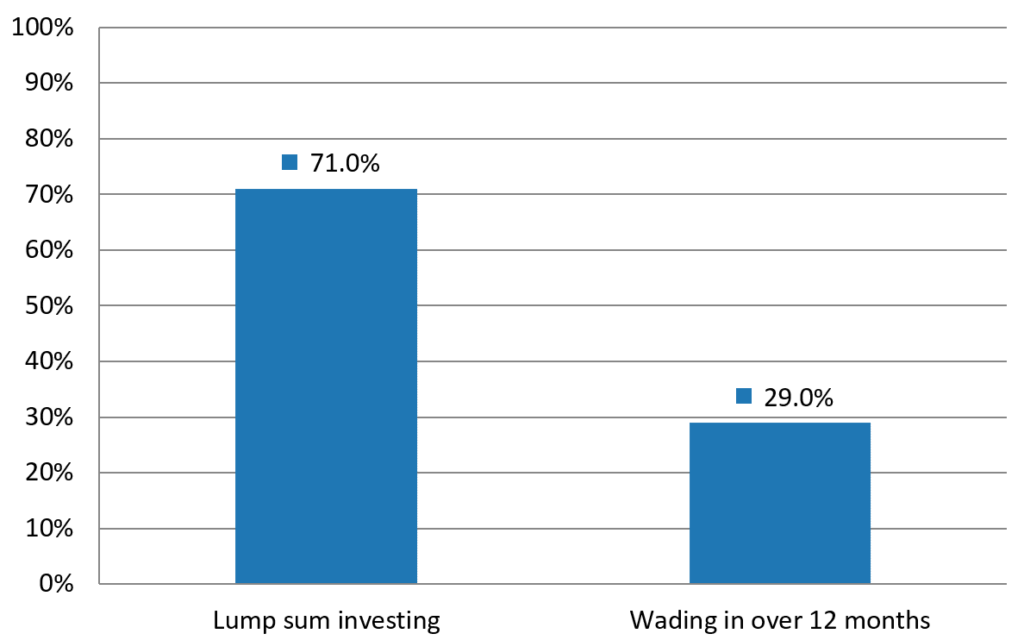

Let’s look at the math behind this decision by seeing which strategy (lump sum investing or dollar cost averaging) would have been the better investment strategy historically. Let’s go all the way back to 1950, and analyze – every month since that time – how a lump sum investment would have performed vs. dollar cost averaging the same aggregate amount over a 12-month period.

The answer is that the lump sum strategy comes out on top 71% of the time. Why is this? The market has always had a generally upward trajectory, and so any day you invest, you have a slight edge (though daily volatility makes this far from obvious). It’s like playing blackjack, except you’re the house. Because of that, the investor who just took the plunge is simply more likely to generate a greater return than the one who wades in slowly. Of course there are some times where dollar cost averaging came out on top, but it’s a minority of the time, and you’re kidding yourself if you think you can correctly call when it’s the right strategy.

One year win-rate:

Lump Sum vs. Wading In

See footnotes below for source and methodology

Lump sum works even better at all-time highs

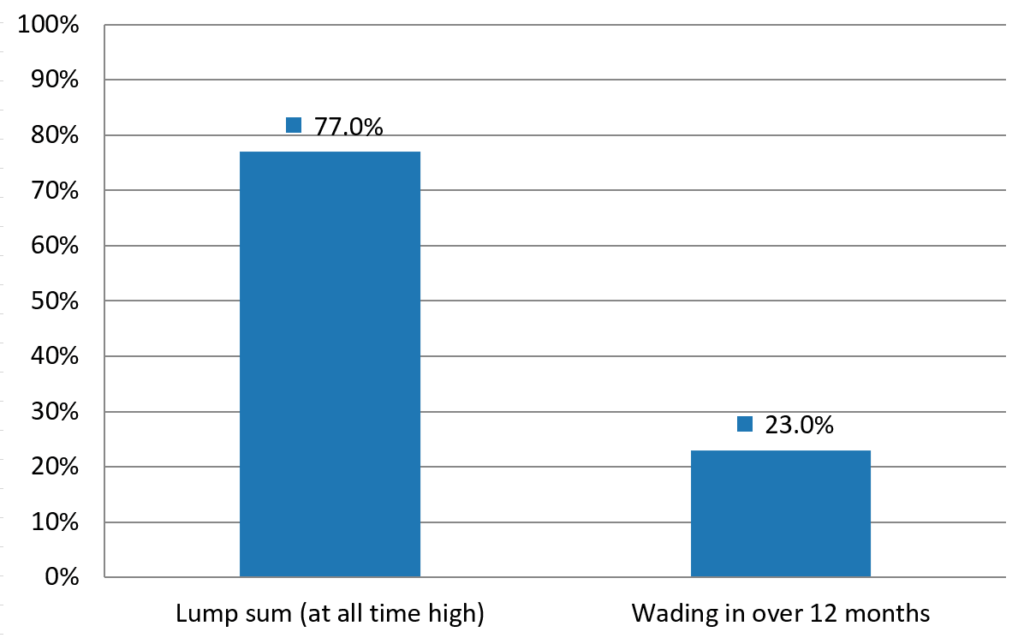

And if we just look at months where the stock market is at an all-time high, those who invested a lump-sum came out ahead 77% of the time!

Why is this? Because all-time highs have not historically been a sign the market is about to crash. Bull markets sometimes run for long stretches. So statistically speaking, all-time highs are more likely to be followed by more all-time highs than when the market is at a low. Further, all-time highs are not uncommon. Again, that’s because the market has a slight upwards bias, it’s how it has to work. Approximately 27% of all months since 1950 have seen an all-time high.

The instinct to wait for a pullback is the instinct that costs you above-average entries.

One year win-rate at all-time highs:

Lump Sum vs. Wading In

See footnotes below for source and methodology

The compounding cost of a cautious strategy

Our law firm partner doesn’t make this decision about his bonus just once in his career. It’s a decision that comes every year, if not every quarter.

So what happens to the cautious lawyer when dollar cost averaging becomes habit?

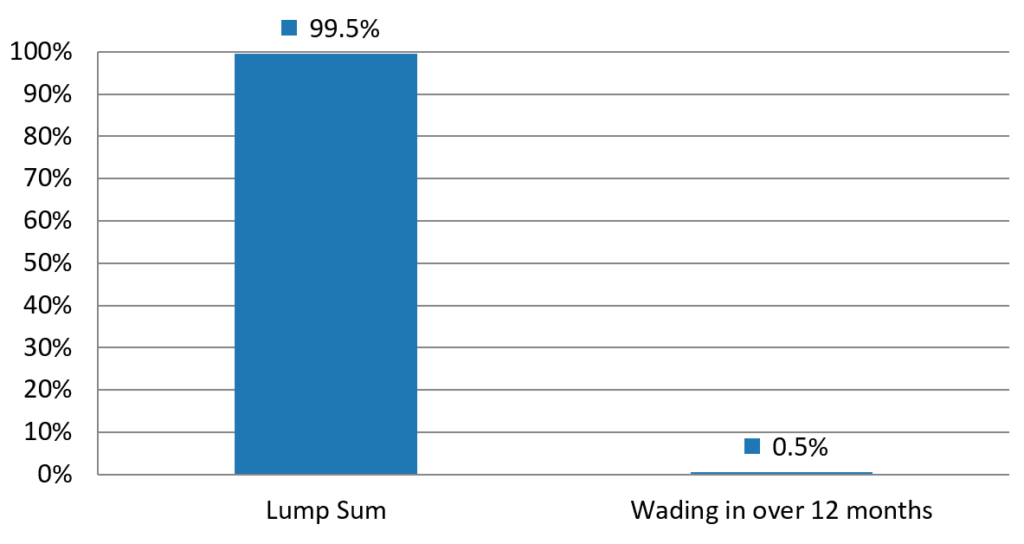

Take the losing bet of dollar cost averaging (with a 29% likelihood of winning) and do that every year for 30 years. The probability that your strategy would outperform a lump sum investing strategy drops to under 0.5%. In other words, just 1 out of 226 lawyers will end up ahead with dollar cost averaging over a 30 year period. Those are terrible odds.

Odds of winning with a 30-year annual strategy

See footnotes below for source and methodology

The fix? Fortune favors the brave!

Jump in the water. Write that check. Get invested. Fortune favors the brave.

If you want to see what that decision looks like with your own numbers, you can run them here:

Takes about 60 seconds.

Source and methodology, chart 1: Robert J. Shiller’s monthly Yale dataset. Across every monthly cohort from January 1950 forward (905 cohorts), a $100,000 lump-sum investment finished ahead of the same amount spread evenly across 12 monthly contributions in 71% of cases. Real total returns, CPI-adjusted, dividends reinvested; no taxes or transaction costs. A link to the Shiller data set used as well as the disclaimers related to this data set can be found at econ.yale.edu/~shiller/data.htm.

Source and methodology, chart 2: Robert J. Shiller’s monthly Yale dataset. Restricting cohort starts to months when the real total-return index closed at or above its prior all-time high (239 cohorts, about 27% of all months since 1950), lump sum still beats 12-month DCA 77% of the time. All-time highs are the typical state of a bull market, not an unusually risky entry point.

Source and methodology for chart 3: Compounding the 29% per-year DCA win rate across 30 independent annual decisions, the probability DCA wins a strict majority of years works out to roughly 0.5% by the binomial distribution — about 1 in 226. The empirical check across 557 historical 30-year career start months since 1950 (Shiller dataset) confirms it: always-lump-sum beats always-DCA in cumulative career-end wealth in 555 of 557 careers.

Disclosure: While historical analysis suggests that lump-sum investing has, in many cases, resulted in higher returns than dollar-cost averaging, investing a large amount at once may subject the investor to immediate market declines, increased short-term volatility, and potential loss of principal, particularly if markets decline shortly after investment. Investors should consider their financial situation, risk tolerance, and investment objectives before implementing any strategy.